02/09/2020

The risk premium indicator EMBI (Emerging Markets Bond Index) for Serbia, which is based on dollar-denominated debt and calculated by the renowned American financial institution J.P. Morgan, is no longer to be published as of the last day of August, after more than 15 years. The reason for this is that there are less than 13 months to maturity of the only dollar Serbian eurobond in circulation (which will mature on 28 September 2021). According to J.P. Morgan’s criteria, this is when the bond is excluded from the calculation (revision of data for EMBI calculation is done on the final day of the month).

The fact that EMBI for Serbia based on US-dollar debt is no longer calculated means that there are no dollar Serbian eurobonds in the market. This is the result of our country’s responsible approach to managing public debt. Thanks to favourable monetary and fiscal movements and successful presentation at the international financial market, over the past years Serbia effected early buyback of a substantial part of expensive debt in respect of dollar eurobonds. This expensive debt, involving the FX risk, was replaced by much cheaper financing in euros. In this way, the share of the dollar in public debt contracted, as did the country’s exposure to the FX risk of USD/EUR relations.

After Serbia’s successful presentation at the international financial market with the first issue of the euro-denominated eurobond in June 2019, benchmark data became available on the EMBI risk premium for Serbia based on euro-denominated debt. From end-July 2019 (since when data are available), this indicator was on average 10 bp lower than the general (composite) global risk premium indicator for emerging economies, which confirms that international investors view Serbia as a safe and favourable investment destination.

The US-dollar EMBI risk premium, calculated as the weighted spread between yield rates on eurobonds of emerging economies and yield rates on US bonds of comparable maturity, is considered the benchmark risk premium indicator of emerging economies. Now that this indicator is no longer published for Serbian US-dollar securities, we have the opportunity to look back at movements in the Republic of Serbia’s risk premium in the past 15 years and compare it with the dynamics of this indicator in other emerging economies.

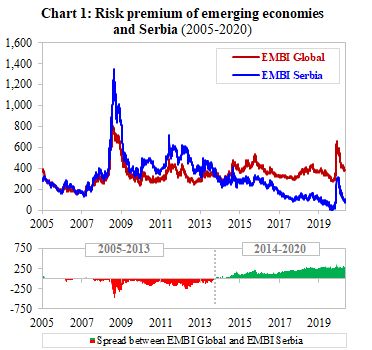

When EMBI Serbia is compared with the composite EMBI Global (which provides information on the general (global) risk premium of emerging economies), two sub-periods stand out clearly (Chart 1) in the past 15 years (2005–2020).).

In this sub-period EMBI Serbia averaged 406 bp, running significantly above the average composite measure for emerging markets (EMBI Global), which equalled 318 bp. During as much as 86% of this sub-period, EMBI Serbia was above EMBI Global, indicating that investors perceived Serbia as a riskier issuer, riskier country and a riskier investment destination on the whole.

Insufficiently entrenched macroeconomic stability also contributed to a more dynamic growth in EMBI Serbia relative to the emerging markets’ average during crisis episodes – first during the Global Economic Crisis (2007–09), when Serbia’s risk premium hit the maximum 1,351 bp, and then during the eurozone sovereign debt crisis (2011–12) as well. In times of heightened uncertainty in financial markets, international investors would lose confidence and would tend to sell Serbia’s dollar-denominated eurobonds more than the eurobonds issued by other emerging economies.

The downward trend in EMBI Serbia began as far back as in the second half of 2013. In the last seven years (from early September 2013 to end-August 2020), EMBI Serbia plummeted by 357 bp (from 460 bp to 103 bp), recording the sharpest decrease among 43 emerging economies. In the same period, EMBI Global went up by 10 bp. It is clear that the fall in the risk premium on Serbia’s dollar-denominated debt over the last seven years is attributable exclusively to domestic factors – the delivery and maintenance of macroeconomic stability, which gave rise to investor confidence.

After the spread between EMBI Serbia and EMBI Global narrowed in early 2014, Serbia’s risk premium has moved constantly below the global risk premium. In this sub-period, EMBI Global averaged 372 bp, while EMBI Serbia averaged 196 bp, which is much lower. The lowest level of EMBI Serbia was recorded on 23 December 2019 (only 5 bp).

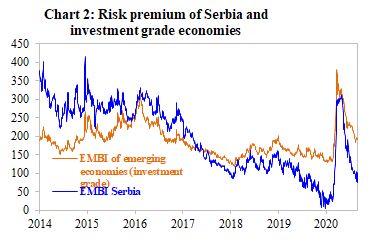

The analysis of dollar EMBI for Serbia and the average risk premia of emerging economies with investment grade credit rating (minimum BBB- according to Standard&Poor’s) shows that from 2017 onwards Serbian dollar-denominated eurobonds were traded in the secondary market under terms typical for countries with investment grade. In other words, professional investors have put Serbia during this period among countries enjoying investment grade, i.e. countries that are safe to invest in, which only illustrates the high confidence of market participants in the macroeconomic prospects of our country.

Governor's Office